Capital Structure Decides Survival

Two developers build the same product on the same street. Same unit count, same finishes, same projected rent. One of them is gone in the next downturn and the other buys his note at a discount. Nothing about the buildings explains it.

The difference sits in a document neither of them shows at the ribbon cutting. One borrowed short money against a long asset. The other matched the term of the debt to the time he actually intended to hold. When rates moved and the refinance window slammed shut, the first man had a balloon coming due against a property that could not be sold or refinanced at the number he needed. The building was fine. The loan was not.

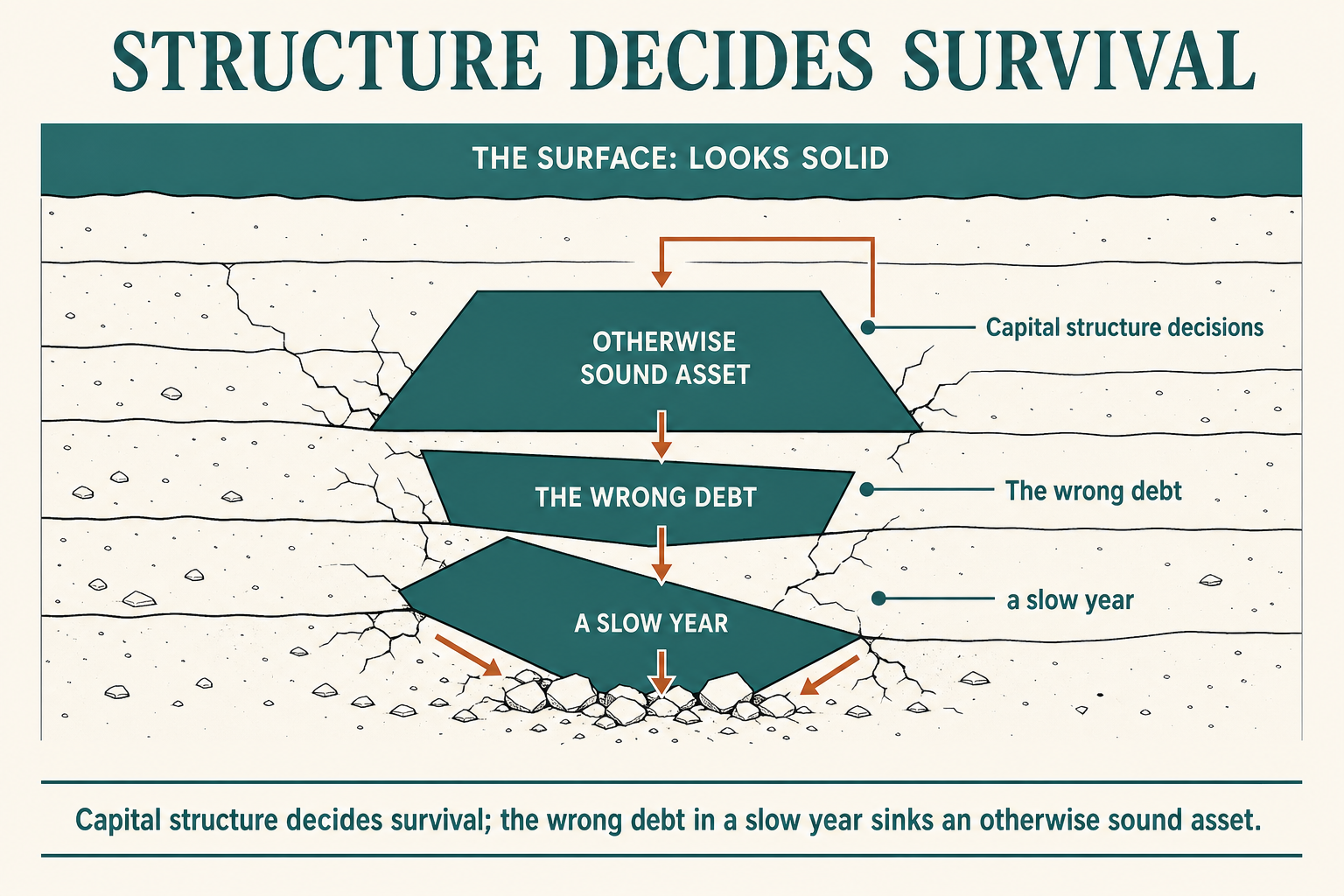

Owners obsess over the asset and barely glance at the structure that funds it.

The Risk You Did Not Underwrite

Most developers underwrite the property carefully and the capital stack carelessly. They model the rent roll to the dollar, stress the vacancy, argue about cap rates. Then they take whatever financing the relationship bank offers and treat it as a settled fact rather than a live variable.

That is backwards. A good building on bad terms is a fragile business. A modest building on terms that match the hold can ride out years of trouble.

The trap is that bad capital structure is invisible while conditions are good. A three-year loan on a property you mean to hold for fifteen looks identical to a fifteen-year loan as long as the refinance market stays open. The gap only shows up when you need to roll the debt and the door is closed. By then you are not negotiating. You are explaining to a special-servicer why he should be patient.

A good building on bad terms is a fragile business.

Match The Money To The Hold

Start with one question, and ask it before you pick finishes, before you pick a contractor, before you fall in love with the pro forma. How long do I actually intend to hold this?

Everything in the capital stack should answer to that number. The term of the debt, the rate type, the amortization, the covenants, the personal guarantees. If the hold is long and patient, the money should be long and patient. If you are building to sell inside eighteen months, short and cheap is rational. The failures come from the mismatch, long-hold intentions funded by short-hold money, because short-hold money is cheaper today and the spread feels like free margin.

It is not free. It is a bet that the refinance window stays open on your schedule. You do not control that window. The rate environment controls it, the lender's appetite controls it, the comparable sales in your submarket control it. You are short a thing you cannot price.

Think of the stack in three layers, each tested against the same hold.

- The senior debt: Does the term run past the next plausible downturn, or do you have to refinance into the teeth of one? A loan that matures in a soft market is not a loan, it is a forced sale with extra steps.

- The rate exposure: If rates move against you, does the deal still cover its debt service, or does it only work at today's number? A deal that only works at one rate is a deal with no margin for being wrong.

- The guarantees and recourse: When this asset gets in trouble, what else gets pulled in with it? An owner who pledged everything to save fifty basis points learns the price of that fifty in a single bad year.

The point is not to avoid leverage. Leverage builds real estate. The point is to size and shape the leverage so a bad eighteen months is survivable rather than terminal.

A deal that only works at one rate is a deal with no margin for being wrong.

The Decision You Make Upstream

There is a property near Round Top, Texas, built around how a group actually uses a place over a weekend, where people gather, where someone drinks coffee in the morning, where the group lands at sunset. The expensive choices were made early. Large shared spaces, real materials with weight to them, sightlines that cost more than the cheap version. Those decisions could not be added later. They had to be right before a single finish was chosen.

Capital structure works the same way. The terms are set at the front, and they govern everything that happens for years afterward. You do not get to re-cut the loan once the cycle turns, the same way you do not get to add ceiling height after the roof is on. The upstream decision is the one that decides whether the downstream story holds.

The owner who refuses the cheap structural shortcut pays more at closing and sleeps through the downturn. The owner who took the easy money looks identical right up until the moment he does not.

You do not get to re-cut the loan once the cycle turns.

How To Tell If The Structure Will Hold

Before you sign, run the deal against the conditions you do not want to imagine.

- The hold question: How long do I actually intend to own this, honestly, and does the term of my debt run at least that long or past the next likely downturn?

- The forced-roll test: If I had to refinance in the worst eighteen months of the next ten years, could I, and at what cost to my equity?

- The one-rate test: Does this deal cover its debt service only at today's rate, or does it still work if rates move two points against me?

- The contagion check: When this single asset gets in trouble, what guarantees, cross-collateral, or recourse pull the rest of my portfolio in with it?

- The cheap-spread question: Where did I take short or floating money because it was cheaper, and am I being paid enough for the risk I just absorbed?

- The patience test: If my lender wanted to be difficult at exactly the wrong moment, how much room would I have to wait him out?

The building is the part you can see, and the part that rarely kills you. The structure that funds it is invisible, and it decides whether you are standing when the cycle turns.

Underwrite the loan with the same discipline you underwrite the rent roll. The asset survives a downturn on the terms it was financed with, not the terms you wish you had.