Underwrite the Reality, Not the Headline

A broker sends you a one-page summary. It names a price, a cap rate, and three comparable sales, all stabilized, all in the same submarket, all built in the last eight years. The math is clean. The cap rate sits where you expected. On paper, the deal underwrites.

Then you visit. You stand in the parking lot of one comp, then the next, then the one you are buying. They are not the same building. One has light that moves through the main spaces. One has the cheapest version of every finish, hidden behind a good photographer. One was built around how people actually use it. The summary flattened all three into a single number, and the number told you almost nothing about which is which.

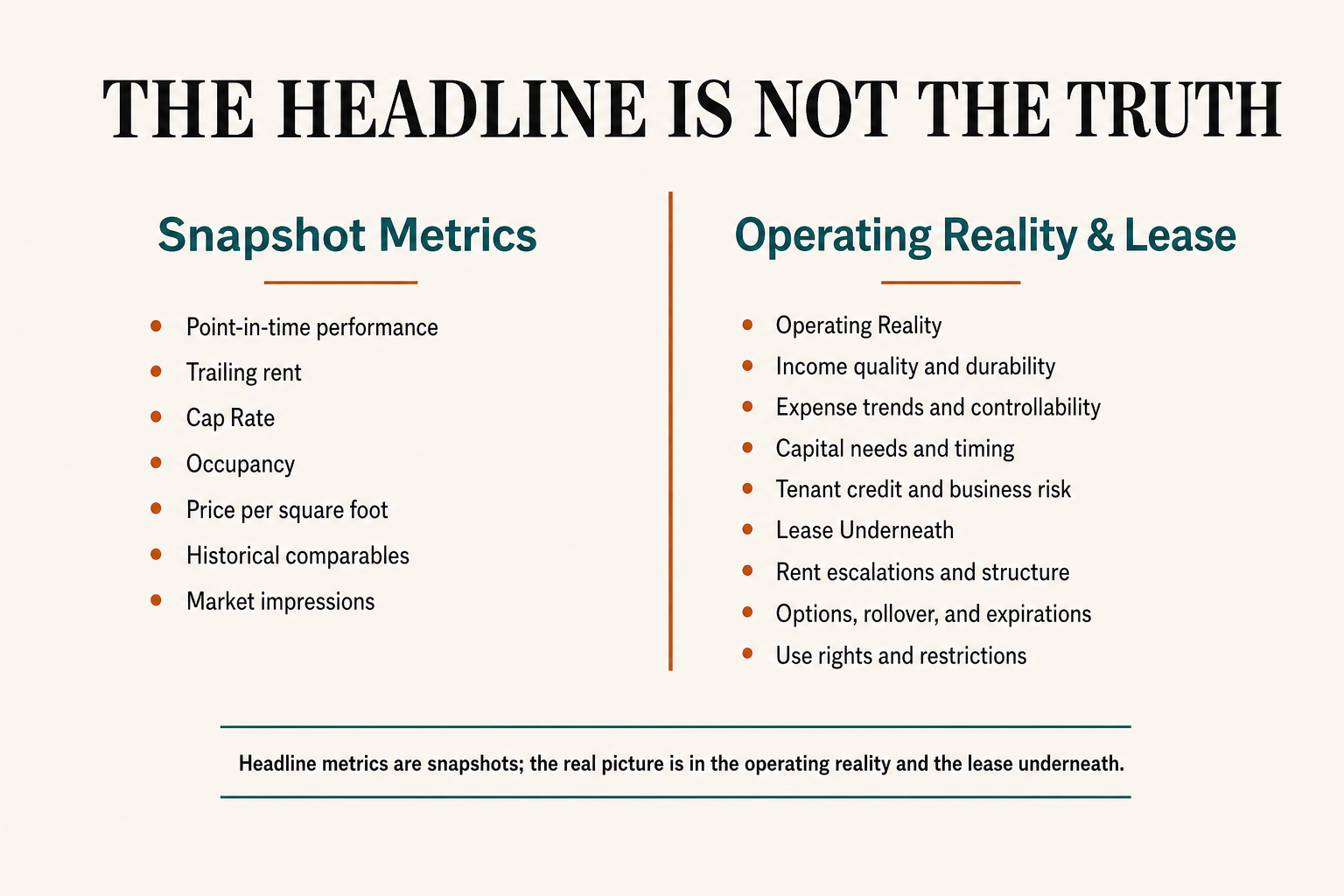

The Number Hides the Asset

A cap rate is a snapshot. It captures one moment of net operating income against one moment of price, and it says nothing about how either was produced or how long either will hold.

Two properties can show the identical cap rate. One earns its income from a building people want to be in, with rents that renew because the experience holds up. The other earns the same income from concessions, deferred maintenance, and a tenant base that is one better option away from leaving.

The number is the same. The asset is not.

The comp set makes this worse, because comps are sold as evidence of sameness. Three sales at the same price per unit look like proof of a market rate. But the comp set treats distinct assets as interchangeable, and the differences that matter most are exactly the ones a spreadsheet cannot hold: how the place feels, how it was built, whether the income is structural or borrowed from the future.

A cap rate tells you what an asset earned last year. It does not tell you what kind of asset earned it.

Underwrite What Produces the Income

The discipline is to stop underwriting the headline and start underwriting the thing that produces it. The number is an output. The asset is the input. If you cannot explain why the income exists, you cannot defend it.

Three questions separate a real asset from a number that happens to match one.

First, is the income structural or borrowed? Structural income comes from a property people choose and renew. Borrowed income comes from concessions, from rents pushed past what the building supports, from maintenance deferred into next year's problem. Same NOI today. Very different NOI in thirty-six months.

Second, what was built into the asset versus painted onto it? Some quality is in the bones: the layout, the sightlines, the materials where they carry weight. Some quality is in the staging: the furniture, the photography, the listing copy. The first holds up when a guest or tenant walks in. The second collapses on contact.

Third, what does it cost to defend the number? A weak asset holds its cap rate only with constant spend: turnover, concessions, marketing to replace people who leave. A strong asset holds it with less, because people stay. The headline cap rate does not show you the cost of keeping it.

This is where most bad deals are made. Not in the math, which is usually correct, but in the assumption that a matching number means a matching asset. The buyer underwrites the comp, inherits its problems, and discovers a year in that he bought the expensive version of someone else's borrowed income.

You are not buying the cap rate. You are buying whatever has to keep being true for the cap rate to survive.

Where the Difference Is Built

We learned this building a property, not buying one, but the lesson runs the same direction.

Element Ranch sits on roughly forty acres near Round Top, Texas. The easy version was obvious: a big house, trendy furniture, call it a ranch retreat, photograph it well, list it. That path produces a commodity. It commands a commodity rate, and it depends entirely on the photos outperforming the reality.

We refused that. Before a single finish was chosen, the design started with how a group actually uses the place over a weekend. Where they gather. Where someone has coffee alone in the morning. Where the group lands at sunset. That decision drove the layout, the pool area, the shared spaces, and the scale. It cost more, because large common spaces and strong sightlines are not the cheap way to build.

The payoff is not visible in a comp. It shows up at evening arrival, when the property opens off the road and the light moves through the living spaces out toward the pool and the land. Guests feel it before they can name it. They call it special, peaceful, different.

That feeling is why the property commands a rate well above comparable rural listings. On a comp sheet, it would sit beside houses with the same bedroom count and look like an outlier. The sheet would be wrong.

Guests do not rent bedrooms. They rent a setting and a level of execution, and that never shows up in the comp.

What to Check Before You Sign

The cap rate and the comp set are the start of the work, not the end of it. Before you trust a headline, go find what produces it.

- Walk it before you model it. Stand in the asset and in every comp. If they feel different in person, your spreadsheet is lying to you, and you should trust your feet.

- Trace the income to its source. Is the NOI built on people who choose to stay, or on concessions and deferred spend that borrow from next year?

- Separate the bones from the staging. Ask what is built into the asset and what is painted on. The painted layer does not survive a tenant or guest walking through the door.

- Price the cost of defense. What does it take to hold this number for three more years? A weak asset is expensive to keep at par.

- Find the comp that is actually unlike the others. If one comp is doing something the rest cannot copy, the comp set is not a comp set. It is one real asset and a crowd of near-misses.

- Ask what the seller stopped doing. Income looks healthiest right before the deferred work comes due.

A number tells you what happened. The asset tells you whether it will keep happening, and only one of those is for sale.

Underwrite the building, the income, and the experience that produces them. The headline is just where you start looking.